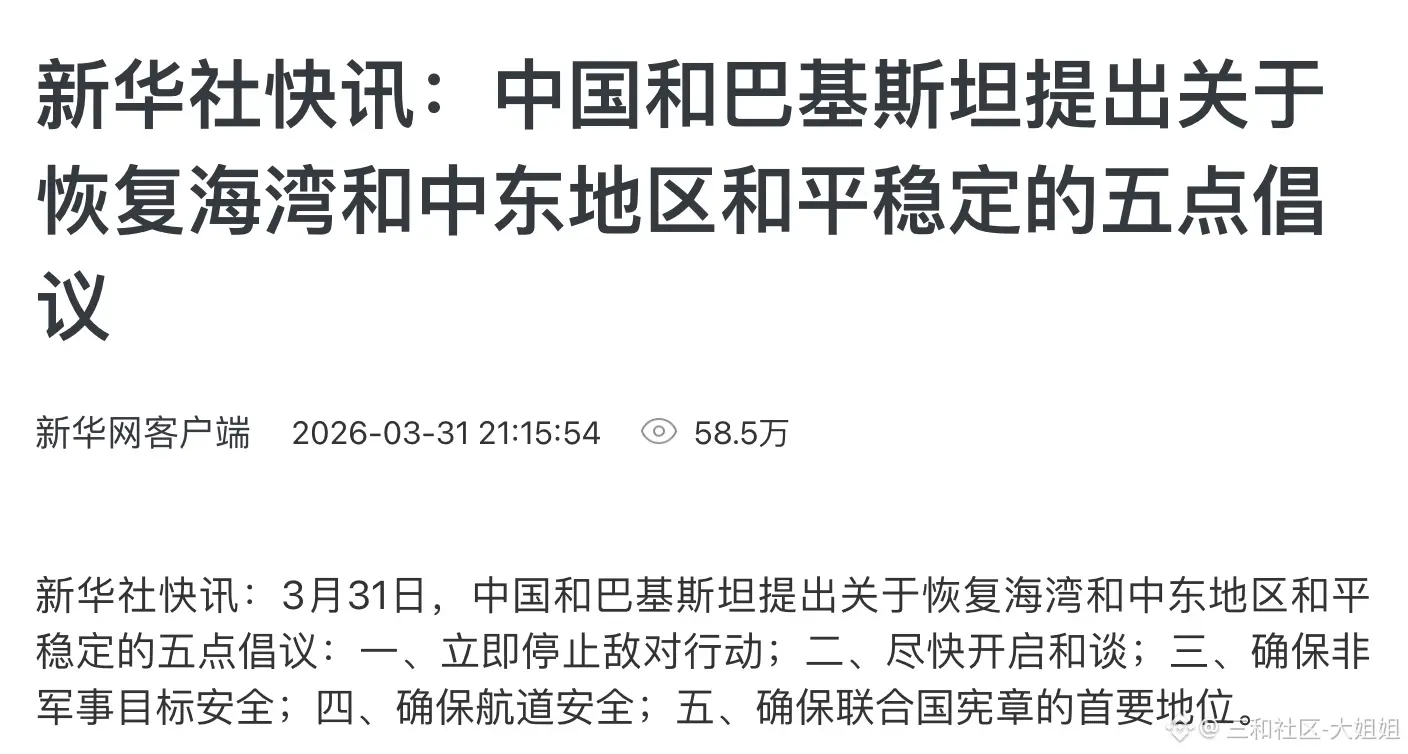

#Gate广场四月发帖挑战 Gold Plunge, Crude Oil Soars: Global Commodities Face a "Wild Battle" Between Bulls and Bears

Trump's speech stirs the global commodities market. On April 2, international gold prices sharply dropped around 9:00 AM, turning from gains to losses, with the lowest touching approximately $4,649 per ounce. Meanwhile, Brent crude oil broke through $106 per barrel strongly, rising over 5% intraday. Prior to this, risk aversion sentiment warmed up, and international gold prices steadily climbed to the $4,800 level this week.

Institutional analysts say that the pricing logic of geopolitical risks is fracturing, and the market has entered a "fast in, fast out" trading mode. Volatility risk is becoming a key variable testing investors' risk management capabilities.

As Trump declared that "the United States will conduct extremely fierce strikes on Iran in the next two to three weeks," this commodities game dominated by geopolitical tensions may continue to exhibit high volatility risks.

Gold as a safe haven is changing, with intense bulls and bears battles. According to Xinhua News Agency, U.S. President Trump delivered a speech on the evening of April 1 (Beijing time, April 2 morning), claiming a "quick, decisive, overwhelming victory" in the Iran conflict. Subsequently, global assets experienced sharp fluctuations, with gold leading the way. As of press time, spot gold was at $4,673 per ounce; COMEX gold futures fell 2.6%, at $4,688 per ounce. Previously, international gold prices had risen for four consecutive days.

"Today's abnormal movement in the gold market is not just a simple technical correction," said a trading professional. He noted that gold prices just recovered the $4,800 mark, only to perform a "big dive" minutes after Trump's speech, reflecting the current market's fragile and speculative capital. Both bullish and bearish funds are showing rapid entry and exit trends, significantly amplifying gold's volatility.

Dongwu Securities analysts pointed out that the current market pricing of geopolitical risks shows a clear "pulsed" characteristic: news triggers sharp rises, while expectations of fulfillment or turning points lead to stampede-like exits.

Shenwan Hongyuan Futures Research Institute believes that although short-term pressure on precious metals has eased, the market has not formed a consensus for a one-sided rally. The fierce battle between profit-taking and safe-haven buying has caused intraday fluctuations to expand sharply.

Huatai Securities forecasts that recent gold price declines are mainly due to liquidity squeezes, as investors tend to hold cash when facing risks. Assets like gold are also facing sell-offs.

A similar macro scenario can be referenced to the 1973-1975 oil crisis, during which gold prices experienced two declines and two rises. The liquidity squeeze caused by risk aversion and economic recession was the main reason for the decline in gold prices.

Regarding the future of gold prices, institutional opinions are notably divided.

Copper Crown Jin Yuan Futures pointed out that, based on recent gold price strength relative to silver, the market's "stagnant rally" logic is gradually approaching. However, it is still too early to conclude that the correction in precious metals has ended, and the gold-silver ratio is expected to further improve.

On the other hand, Goldman Sachs maintains its long-term bullish stance, expecting gold to rise to $5,400 per ounce by the end of 2026. However, Goldman also warns that if the Hormuz Strait remains disrupted, gold could face further short-term selling pressure.

Additionally, institutions have simulated the subsequent trend of the conflict. Even if the geopolitical event ends, it may not necessarily be a purely bearish signal for gold. IG market analyst Tony Sycamore said that if the conflict ends, it could be a double-edged sword for gold. On one hand, a lasting peace agreement could weaken the geopolitical safe-haven demand that supported gold during the war; on the other hand, if oil prices fall and inflation pressures ease, market expectations of Fed rate cuts in 2026 could re-emerge, potentially supporting gold.

Geopolitical premiums lift oil prices, with institutions stating "can't go back below $65"

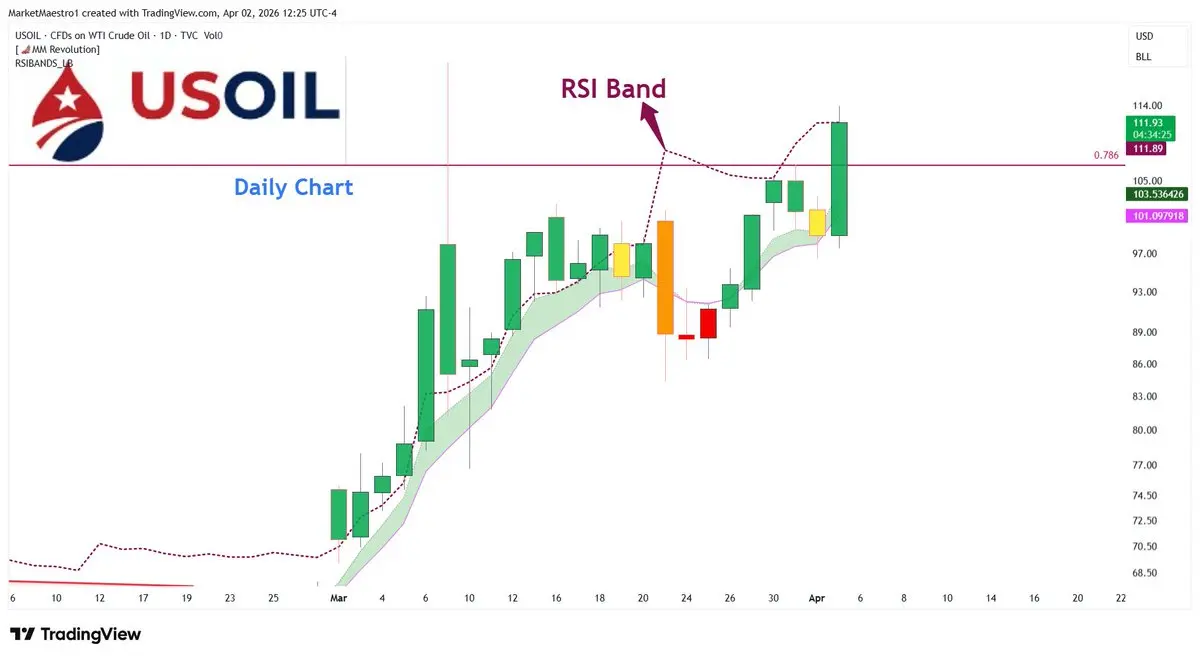

Compared to the sharp fluctuations in gold, the oil market appears "more directional and energetic." On April 2, Brent crude oil broke through $106 per barrel, surging 4.78% intraday. The geopolitical premium has raised the oil price center. During this rally, WTI crude oil futures climbed from around $65 per barrel, reaching a high of $113 in March, with a monthly increase of 51% and an year-to-date gain of 83%.

Robert Reini, head of commodities research at Westpac Banking Corporation, analyzed: "Trump's speech did not change the fundamental reality— the Strait has been effectively closed for a month, and oil flow remains severely restricted. Disruptions could still occur in the coming weeks or longer." He added that Brent crude oil is expected to trade between $95 and $110 per barrel in the short term.

According to CCTV News, on April 1, U.S. President Trump stated that the U.S. no longer needs the Hormuz Strait, nor does it need it now. For countries that rely on the Strait to access oil, Trump urged them to either "buy oil from the U.S." or directly "grab oil" through the Strait. "Even if there's a ceasefire tomorrow, prices won't go back," is the common consensus among market institutions on oil pricing.

Andy Lipo, president of Lipo Petroleum Consulting, believes that even if the conflict ends tomorrow, oil prices could immediately fall by $10 to $15, but they will not return to the pre-conflict level of around $65. The market has already begun to price in higher geopolitical risk premiums in the Middle East.

Copper Crown Jin Yuan Futures further analyzed that current geopolitical signals are still switching back and forth, with significant divergence in market expectations. Even if the Middle East conflict ends, concerns about prolonged high oil prices disrupting the global economy remain strong, making it difficult for oil prices to return to previous levels.

Moreover, supply chain wounds are unlikely to heal quickly. Shenwan Hongyuan Futures believes that even if the Strait reopens immediately, restoring the entire supply system will take time, including repositioning oil tankers, adjusting routes, restoring capacity, and restarting refineries, all requiring a long recovery cycle. Although geopolitical tensions have shown signs of "cooling," this is likely just verbal easing, with substantial disagreements still unresolved and high uncertainty.

Pay attention to "Trump's rhythm" and beware of tail risks

In the face of current market volatility driven by geopolitics, many institutions believe that the global asset pricing logic is shifting and have proposed new strategies.

Dongwu Securities mentioned in a research report that the current market's rise and fall are heavily influenced by overseas factors, especially the so-called "TACO" rhythm (alternating escalation and de-escalation of conflicts) triggered by Trump's speeches. They advise investors to wait for clearer developments before making further investment decisions.

Shenwan Hongyuan Futures recommends from a risk hedging perspective that if there is no substantive progress in peace talks or if conflicts unexpectedly escalate in the coming weeks, oil prices could spike again. Investors should closely monitor US-Iran diplomatic feedback and the movements of U.S. ground forces. As for gold, given its long-term upward trend, short-term volatility may actually provide opportunities for medium- and long-term allocation. Most statistical agencies warn that within the "next two to three weeks," volatility trading in gold and the restructuring of geopolitical premiums in oil will be two core focuses for global investors, with high tail risks to watch out for.

Huatai Securities emphasizes that managing investment pace during risk events is crucial. The report notes that, according to CFTC positioning data, net long positions of asset management institutions have decreased by 32% from 134,000 contracts on January 13 to 91,000 contracts on March 24, near a one-year low, suggesting marginal selling pressure may be easing. The report further warns that before the Strait reopens and the oil dollar cycle resumes, investors should remain cautious of liquidity squeeze risks similar to those in mid-1974.

Yao Yuan, senior investment strategist at Oriental Horizon Asset Management's Asia Research Institute, advises investors to distinguish between short-term trading and long-term allocation.

In the short term, geopolitical conflict evolution is unpredictable. Over-allocating to risk assets should involve reducing exposure, increasing cash holdings, and hedging through energy, commodities, and derivatives. For long-term allocation, Yao recommends using gold and physical assets to hedge structural geopolitical risks, increasing positions in Europe and emerging markets to counteract U.S. retreat effects, and diversifying into AI and energy transition sectors.

Trump's speech stirs the global commodities market. On April 2, international gold prices sharply dropped around 9:00 AM, turning from gains to losses, with the lowest touching approximately $4,649 per ounce. Meanwhile, Brent crude oil broke through $106 per barrel strongly, rising over 5% intraday. Prior to this, risk aversion sentiment warmed up, and international gold prices steadily climbed to the $4,800 level this week.

Institutional analysts say that the pricing logic of geopolitical risks is fracturing, and the market has entered a "fast in, fast out" trading mode. Volatility risk is becoming a key variable testing investors' risk management capabilities.

As Trump declared that "the United States will conduct extremely fierce strikes on Iran in the next two to three weeks," this commodities game dominated by geopolitical tensions may continue to exhibit high volatility risks.

Gold as a safe haven is changing, with intense bulls and bears battles. According to Xinhua News Agency, U.S. President Trump delivered a speech on the evening of April 1 (Beijing time, April 2 morning), claiming a "quick, decisive, overwhelming victory" in the Iran conflict. Subsequently, global assets experienced sharp fluctuations, with gold leading the way. As of press time, spot gold was at $4,673 per ounce; COMEX gold futures fell 2.6%, at $4,688 per ounce. Previously, international gold prices had risen for four consecutive days.

"Today's abnormal movement in the gold market is not just a simple technical correction," said a trading professional. He noted that gold prices just recovered the $4,800 mark, only to perform a "big dive" minutes after Trump's speech, reflecting the current market's fragile and speculative capital. Both bullish and bearish funds are showing rapid entry and exit trends, significantly amplifying gold's volatility.

Dongwu Securities analysts pointed out that the current market pricing of geopolitical risks shows a clear "pulsed" characteristic: news triggers sharp rises, while expectations of fulfillment or turning points lead to stampede-like exits.

Shenwan Hongyuan Futures Research Institute believes that although short-term pressure on precious metals has eased, the market has not formed a consensus for a one-sided rally. The fierce battle between profit-taking and safe-haven buying has caused intraday fluctuations to expand sharply.

Huatai Securities forecasts that recent gold price declines are mainly due to liquidity squeezes, as investors tend to hold cash when facing risks. Assets like gold are also facing sell-offs.

A similar macro scenario can be referenced to the 1973-1975 oil crisis, during which gold prices experienced two declines and two rises. The liquidity squeeze caused by risk aversion and economic recession was the main reason for the decline in gold prices.

Regarding the future of gold prices, institutional opinions are notably divided.

Copper Crown Jin Yuan Futures pointed out that, based on recent gold price strength relative to silver, the market's "stagnant rally" logic is gradually approaching. However, it is still too early to conclude that the correction in precious metals has ended, and the gold-silver ratio is expected to further improve.

On the other hand, Goldman Sachs maintains its long-term bullish stance, expecting gold to rise to $5,400 per ounce by the end of 2026. However, Goldman also warns that if the Hormuz Strait remains disrupted, gold could face further short-term selling pressure.

Additionally, institutions have simulated the subsequent trend of the conflict. Even if the geopolitical event ends, it may not necessarily be a purely bearish signal for gold. IG market analyst Tony Sycamore said that if the conflict ends, it could be a double-edged sword for gold. On one hand, a lasting peace agreement could weaken the geopolitical safe-haven demand that supported gold during the war; on the other hand, if oil prices fall and inflation pressures ease, market expectations of Fed rate cuts in 2026 could re-emerge, potentially supporting gold.

Geopolitical premiums lift oil prices, with institutions stating "can't go back below $65"

Compared to the sharp fluctuations in gold, the oil market appears "more directional and energetic." On April 2, Brent crude oil broke through $106 per barrel, surging 4.78% intraday. The geopolitical premium has raised the oil price center. During this rally, WTI crude oil futures climbed from around $65 per barrel, reaching a high of $113 in March, with a monthly increase of 51% and an year-to-date gain of 83%.

Robert Reini, head of commodities research at Westpac Banking Corporation, analyzed: "Trump's speech did not change the fundamental reality— the Strait has been effectively closed for a month, and oil flow remains severely restricted. Disruptions could still occur in the coming weeks or longer." He added that Brent crude oil is expected to trade between $95 and $110 per barrel in the short term.

According to CCTV News, on April 1, U.S. President Trump stated that the U.S. no longer needs the Hormuz Strait, nor does it need it now. For countries that rely on the Strait to access oil, Trump urged them to either "buy oil from the U.S." or directly "grab oil" through the Strait. "Even if there's a ceasefire tomorrow, prices won't go back," is the common consensus among market institutions on oil pricing.

Andy Lipo, president of Lipo Petroleum Consulting, believes that even if the conflict ends tomorrow, oil prices could immediately fall by $10 to $15, but they will not return to the pre-conflict level of around $65. The market has already begun to price in higher geopolitical risk premiums in the Middle East.

Copper Crown Jin Yuan Futures further analyzed that current geopolitical signals are still switching back and forth, with significant divergence in market expectations. Even if the Middle East conflict ends, concerns about prolonged high oil prices disrupting the global economy remain strong, making it difficult for oil prices to return to previous levels.

Moreover, supply chain wounds are unlikely to heal quickly. Shenwan Hongyuan Futures believes that even if the Strait reopens immediately, restoring the entire supply system will take time, including repositioning oil tankers, adjusting routes, restoring capacity, and restarting refineries, all requiring a long recovery cycle. Although geopolitical tensions have shown signs of "cooling," this is likely just verbal easing, with substantial disagreements still unresolved and high uncertainty.

Pay attention to "Trump's rhythm" and beware of tail risks

In the face of current market volatility driven by geopolitics, many institutions believe that the global asset pricing logic is shifting and have proposed new strategies.

Dongwu Securities mentioned in a research report that the current market's rise and fall are heavily influenced by overseas factors, especially the so-called "TACO" rhythm (alternating escalation and de-escalation of conflicts) triggered by Trump's speeches. They advise investors to wait for clearer developments before making further investment decisions.

Shenwan Hongyuan Futures recommends from a risk hedging perspective that if there is no substantive progress in peace talks or if conflicts unexpectedly escalate in the coming weeks, oil prices could spike again. Investors should closely monitor US-Iran diplomatic feedback and the movements of U.S. ground forces. As for gold, given its long-term upward trend, short-term volatility may actually provide opportunities for medium- and long-term allocation. Most statistical agencies warn that within the "next two to three weeks," volatility trading in gold and the restructuring of geopolitical premiums in oil will be two core focuses for global investors, with high tail risks to watch out for.

Huatai Securities emphasizes that managing investment pace during risk events is crucial. The report notes that, according to CFTC positioning data, net long positions of asset management institutions have decreased by 32% from 134,000 contracts on January 13 to 91,000 contracts on March 24, near a one-year low, suggesting marginal selling pressure may be easing. The report further warns that before the Strait reopens and the oil dollar cycle resumes, investors should remain cautious of liquidity squeeze risks similar to those in mid-1974.

Yao Yuan, senior investment strategist at Oriental Horizon Asset Management's Asia Research Institute, advises investors to distinguish between short-term trading and long-term allocation.

In the short term, geopolitical conflict evolution is unpredictable. Over-allocating to risk assets should involve reducing exposure, increasing cash holdings, and hedging through energy, commodities, and derivatives. For long-term allocation, Yao recommends using gold and physical assets to hedge structural geopolitical risks, increasing positions in Europe and emerging markets to counteract U.S. retreat effects, and diversifying into AI and energy transition sectors.