As the US-Israeli coalition escalates military actions against Iran, Tehran’s years-long “shadow economy” has once again become an international focus. This parallel system, combining Bitcoin mining and stablecoin trading, has become Iran’s last shield in seeking survival outside the battered banking system and dollar dominance.

Exchanging cheap electricity for Bitcoin

Iran legalized cryptocurrency mining as early as 2019, allowing licensed operators to mine using government-subsidized electricity on the condition that all mined Bitcoin must be sold to the Central Bank of Iran. This has become an important tool for paying for imported goods and settling foreign trade, effectively bypassing the US dollar system and Western banking sanctions to some extent.

According to statistics, Iran’s Bitcoin mining hash rate accounts for about 2% to 5% of the global total, but much mining activity remains unofficial, so the actual scale may be higher than reported.

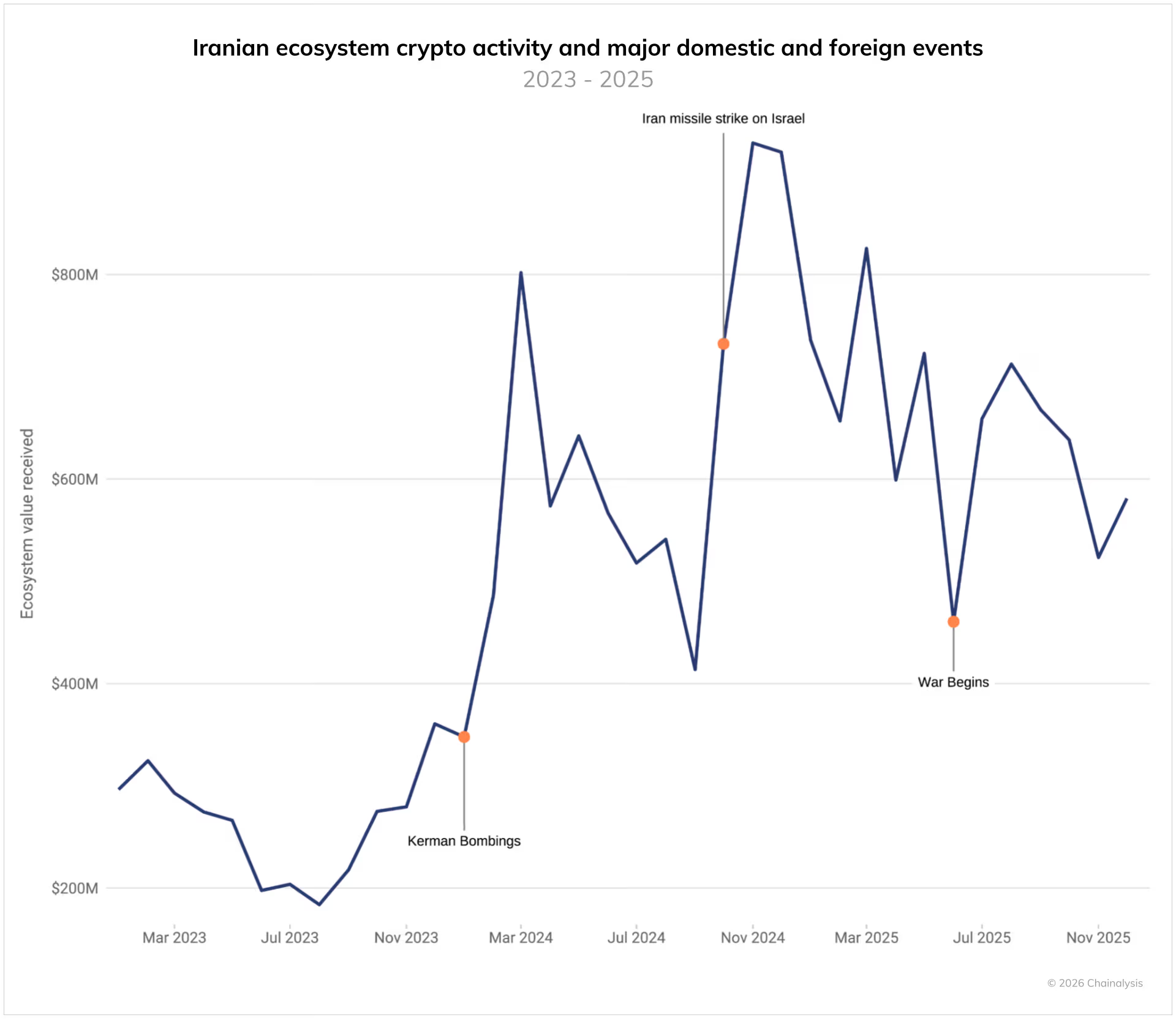

Blockchain analytics firm Chainalysis found that Iran’s cryptocurrency ecosystem had grown to a $7.8 billion scale by 2025, nearly equivalent to the GDP of Maldives or Liechtenstein. Notably, crypto activity tends to spike during military conflicts or domestic unrest, including during last year’s 12-day conflict between Iran and Israel.

As Iran’s main military force, the Islamic Revolutionary Guard Corps (IRGC) has increasingly relied on cryptocurrencies in recent years. Chainalysis estimates that in Q4 2025, wallets associated with the IRGC accounted for over 50% of Iran’s total cryptocurrency inflows, receiving assets worth over $3 billion last year.

These figures only include publicly known wallet addresses directly linked to sanctions lists; the actual scale could be higher.

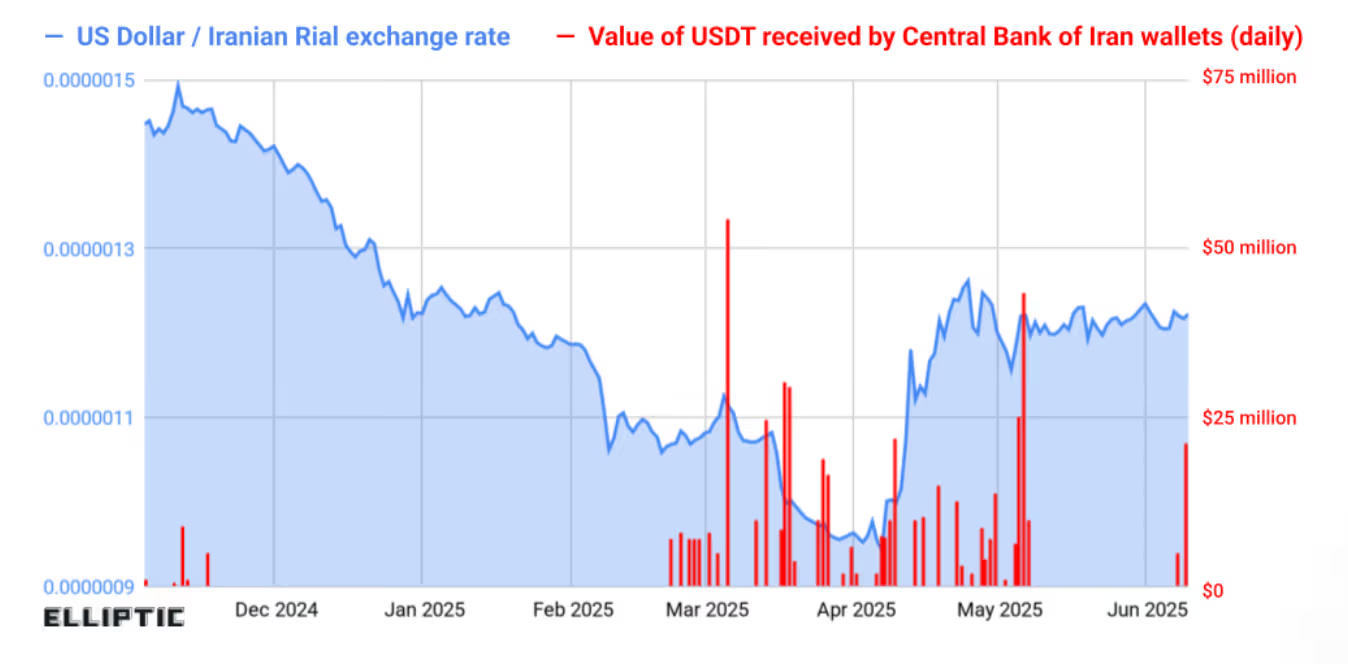

Rial plummets 96%, USDT becomes the new favorite for trade settlement

Besides Bitcoin, stablecoins also play a key role. Elliptic, a blockchain analysis firm, indicated that by 2025, Iran’s central bank had accumulated at least $507 million in USDT, likely used to stabilize the Rial exchange rate and support foreign trade. However, this financial defense appears to have been largely ineffective, as the Rial has depreciated over 96% against the US dollar.

Faced with deep-rooted hyperinflation and an economy on the brink of collapse, ordinary Iranians are increasingly turning to Bitcoin. Data shows that during recent anti-government protests, the amount of Bitcoin withdrawn from centralized exchanges to personal wallets surged sharply, indicating that locals are trying to keep their assets under their own control.

Mining costs are only about $1,300 per Bitcoin

Estimates suggest that the cost of mining one Bitcoin in Iran is around $1,300. Miners sell the mined Bitcoin to the central bank, which then transfers funds overseas to pay for equipment, fuel, or daily necessities.

Disclaimer: The information on this page may come from third parties and does not represent the views or opinions of Gate. The content displayed on this page is for reference only and does not constitute any financial, investment, or legal advice. Gate does not guarantee the accuracy or completeness of the information and shall not be liable for any losses arising from the use of this information. Virtual asset investments carry high risks and are subject to significant price volatility. You may lose all of your invested principal. Please fully understand the relevant risks and make prudent decisions based on your own financial situation and risk tolerance. For details, please refer to

Disclaimer.

Related Articles

Lebanon says the solution is a ceasefire, followed by direct negotiations with Israel

Gate News message, April 9, Lebanon said today that the solution is to first achieve a ceasefire, followed by direct negotiations with Israel.

GateNews46m ago

The delegations from Iran and the U.S. will hold direct talks in Islamabad, aiming to reach a permanent ceasefire agreement

A Pakistani government source said that representatives from Iran and the U.S. will hold direct talks in Islamabad on April 9, with the goal of reaching a permanent ceasefire agreement. The negotiations will take place in a secure military facility, and are expected to last more than a day.

GateNews1h ago

IMF cuts global economic growth forecast amid Iran war

Gate News update, on April 9, IMF Managing Director Kristalina Georgieva said the IMF has lowered its global economic growth forecast due to the war in Iran.

GateNews1h ago

Poland’s central bank governor: We will continue buying gold, with the target increasing to 700 tons

Gate News message, April 9, the head of the National Bank of Poland, Glapiński, said the National Bank of Poland will continue to buy gold. Glapiński reiterated the target to increase gold reserves to 700 tons; the National Bank of Poland currently holds 580 tons of gold.

GateNews2h ago

Multiple European financial institutions: International oil prices are unlikely to fall back to pre-U.S.-Iran conflict levels in the near term

Multiple European financial institutions predict that international oil prices will be difficult to fall back to pre–U.S.-Iran conflict levels in the short term; attention should be paid to the recovery of the Strait of Hormuz and Middle East infrastructure. Although ceasefire news has eased concerns about supply, oil prices may continue to fluctuate in the future.

GateNews2h ago

The U.S.-Iran negotiations have been inconsistent, and Bitcoin and gold both surged and then fell back.

After the Iran–Israel ceasefire, Bitcoin and gold both rose in sync before pulling back. From the perspective of geopolitical chess, we break down the deeper logic behind the price moves and the outlook that follows.

InstantTrends3h ago