January 30th, the approaching deadline for the U.S. government shutdown puts pressure on Bitcoin after falling below January’s high. Historical data shows that during past four shutdowns, Bitcoin declined three times, with only a technical rebound in 2018 as an exception. Miners’ output plummeted due to winter storms, with MARA decreasing from 45 to 7 BTC, and realized losses increasing, indicating investor panic and exit.

January 30th U.S. Government Shutdown Crisis Reemerges

The risk of a U.S. government shutdown is rising again, primarily because Congress has failed to finalize funding bills for multiple programs for the 2026 fiscal year. Temporary funding expires on January 30th, and negotiations remain deadlocked, especially over Homeland Security appropriations. Senate Minority Leader Schumer publicly opposes the Homeland Security funding plan, further increasing the risk of a partial shutdown.

Unless lawmakers pass a new continuing resolution or full-year appropriations before the deadline, some federal departments will shut down immediately. The market currently views January 30th as a binary macroeconomic event, and this uncertainty is exerting pressure on risk assets. For Bitcoin, this date could become a critical turning point in short-term trend determination.

In January 2026, Bitcoin’s price action has reflected increasing fragility. Mid-month, Bitcoin briefly approached the $95,000 to $98,000 range but failed to hold these levels and sharply retreated. This pattern of failed breakouts is often seen as a sign of weakening trend in technical analysis, indicating insufficient buying momentum to sustain higher prices.

From a market psychology perspective, Bitcoin is under pressure entering this critical period. After a failed rebound in January and a sharp shift in market sentiment, investor confidence has been notably shaken. The U.S. government shutdown adds macroeconomic uncertainty, potentially becoming the last straw for bulls. Historical data shows Bitcoin has not served as a reliable hedge during government shutdowns; instead, its price tends to follow existing market momentum.

Historical Data Reveals Bitcoin’s True Nature During Shutdowns

Bitcoin’s performance during U.S. government shutdowns has almost never supported bullish views. Over the past decade, during four such events, Bitcoin declined three times or continued its downward trend, with only one exception. This 75% decline probability is significant for current markets.

The only exception was in February 2018, during a brief liquidity interruption, when Bitcoin and stocks rebounded in tandem. However, deeper analysis shows that rebound was due to technical oversold conditions, not a response to the shutdown itself. Bitcoin had just crashed from its all-time high at the end of 2017, and the market was severely oversold; the rebound was a natural correction, unrelated to the shutdown.

The overall trend is consistent: government shutdowns tend to exacerbate market volatility rather than steer markets in a particular direction. Bitcoin usually reinforces its existing trend rather than reversing it. This is especially relevant now, as Bitcoin is in a correction phase from a high point, with a downward bias. If historical patterns repeat, the shutdown on January 30th could accelerate this downward momentum.

Why does Bitcoin perform poorly during U.S. government shutdowns? The core reason lies in its asset classification. Although some supporters see it as “digital gold” or a safe haven, market behavior indicates that during macroeconomic uncertainty, it behaves more like a risk asset. Government shutdowns are typically accompanied by liquidity tightening and risk aversion, leading investors to sell high-volatility assets rather than accumulate.

Additionally, the structure of Bitcoin market participants influences its performance during shutdowns. Institutional investors and high-net-worth individuals tend to reduce risk exposure amid political uncertainty, implying they may redeem or sell Bitcoin. Retail investors, being less sensitive to macro events, may delay reactions, but when prices fall, panic selling can further deepen declines.

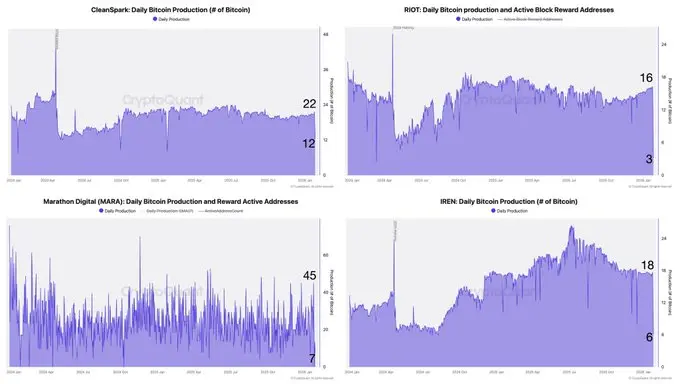

Miner Output Plummets 85%, Exposing Industry Fragility

(Source: CryptoQuant)

Latest on-chain data adds a cautious tone to Bitcoin. According to CryptoQuant, due to winter storms causing grid outages, several major U.S. mining companies have recently sharply reduced their output. CleanSpark’s daily Bitcoin production dropped from 22 to 12 BTC, a 45% decrease. Riot Platforms’ output fell more dramatically, from 16 to 3 BTC, an 81% decline.

Most striking is Marathon Digital (MARA). This “solo mining” operation saw daily production collapse from 45 BTC to just 7 BTC, an 84% decrease. Solo mining tends to be more volatile, but such an almost shutdown-level drop exceeds expectations. Other miners like IREN also reported similar large reductions.

The direct cause of the output decline is extreme weather events. Winter storms hit multiple U.S. states, stressing the power grid. Mining companies have proactively or reactively scaled back operations to support grid stability. This exposes the high dependence of Bitcoin mining on energy infrastructure and its vulnerability to extreme events.

From a supply-demand perspective, reduced miner output should theoretically decrease market supply and support prices. However, historical experience shows that unless demand is strong, miner supply restrictions are insufficient to offset macroeconomic selling pressures. Current demand signals remain weak, ETF fund outflows continue, and retail participation is low. In this environment, temporary supply contraction is unlikely to reverse the price trend.

More concerning is the financial pressure on miners. Reduced production means lower income, while fixed costs (equipment depreciation, rent, labor) remain unchanged. If extreme weather persists or recurs frequently, some financially weaker miners may be forced to sell Bitcoin holdings to maintain cash flow. This passive selling during a fragile market will add further selling pressure.

Realized Losses Rise, Indicating Panic Exit

(Source: CryptoQuant)

Net Realized Profit/Loss (NRPL) data further supports a defensive outlook. Recent weeks have seen an increase in realized losses, meaning more investors are selling Bitcoin below their purchase prices. Compared to early 2025, large-scale profit-taking has decreased, which is not a positive sign but indicates a lack of sufficient floating profits.

The increase in realized losses reflects investors exiting positions at unfavorable prices, not confidently rotating capital. This behavior is typical of late-cycle distribution and de-risking phases, not accumulation. When holders sell at a loss, it suggests expectations of larger future losses or liquidity needs to meet other pressures.

Psychologically, the accumulation of realized losses can create a negative feedback loop. Seeing others exit at a loss can heighten panic, with fears of becoming the last bagholder. This collective panic often peaks during macroeconomic uncertainties like a government shutdown.

NRPL data also implies the market is undergoing a transfer of ownership, but not from weak hands to strong hands. Instead, it’s from loss-makers to cash holders. When large amounts of chips are transacted at a loss, it indicates low confidence in the current price level. This cost basis shift will likely lower future support levels.

In such conditions, negative macro news tends to accelerate downward volatility rather than trigger sustained rallies. The U.S. government shutdown, as a clear negative event, could serve as a catalyst for larger stop-loss cascades.

Three Possible Scenarios for Bitcoin on January 30th

If the U.S. government indeed shuts down on January 30th, Bitcoin is more likely to behave as a risk asset rather than a hedge. Based on historical data and current market structure, three scenarios can be projected.

The most probable is a pessimistic scenario: intense short-term volatility with a downward bias. If it breaks below January’s lows, it aligns with historical shutdown behavior and current market structure. Specific price paths could test support at $90,000, and if broken, accelerate toward $85,000–$88,000. Technically, this would form a deeper correction pattern, possibly requiring weeks to establish a bottom.

A neutral scenario involves the shutdown impact being partially priced in. If the market has already fully discounted the risk before January 30th, the actual event might trigger a short-term relief rally. However, unless overall liquidity improves, such rebounds are likely technical and short-lived. In this case, Bitcoin could oscillate between $90,000 and $95,000, awaiting the next catalyst.

The least likely is an optimistic scenario: a significant rally driven solely by news of the shutdown. Bitcoin rarely rises solely on shutdown news without other positive inflows or sentiment shifts. To reverse the trend upward, large ETF inflows or major positive developments (regulatory breakthroughs or institutional accumulation) are needed.