Futures

Access hundreds of perpetual contracts

TradFi

Gold

One platform for global traditional assets

Options

Hot

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Introduction to Futures Trading

Learn the basics of futures trading

Futures Events

Join events to earn rewards

Demo Trading

Use virtual funds to practice risk-free trading

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Launchpad

Be early to the next big token project

Alpha Points

Trade on-chain assets and earn airdrops

Futures Points

Earn futures points and claim airdrop rewards

More

An Overlooked Supply Shock: 70% of Iran's Steel Production Capacity May Disappear

While the global metals market’s attention is still fixed on aluminum production capacity in the Gulf region, a disruptive shock to the global steel supply-and-demand landscape is being systematically underestimated.

According to CCTV News, Israeli Prime Minister Benjamin Netanyahu said on April 4 local time that the Israeli military carried out strikes on Iran’s steel mills and petrochemical plants that day, and has destroyed 70% of Iran’s steel production capacity.

Iran’s 2025 steel output is approximately 32 million tons, accounting for about 1.8% of global steel output, about 3.8% of global steel output outside China. Its scale is comparable to Germany (34 million tons), about 40% of the United States’ (82 million tons) output, and one quarter of overall European output (134 million tons)—this is by no means a marginal player. If 70% of capacity has indeed been destroyed, more than 20 million tons of annual capacity will evaporate from the market.

Citi warns that this is a structural supply gap that the market has severely underestimated, and the global steel supply-and-demand balance will face a substantive reshaping.

The core pillar of the Middle East steel map

The rise of Iran’s steel industry is of high strategic significance.

According to data from the World Steel Association, Iran’s annual steel production has grown from 14.4 million tons in 2013 to 32 million tons in 2025; over 13 years it has doubled, with a compound annual growth rate of 6.3%, placing it among the world’s top ten steel-producing countries. Thirty percent of Iran’s steel output is used for exports, while 70% satisfies domestic demand, forming a supply pattern that balances both domestic and international markets.

The core impact of this strike lies in: if domestic capacity is sharply reduced, the portion of output that was originally earmarked for exports will prioritize meeting domestic demand—meaning that the 9 million tons of net export volume will almost inevitably quickly exit global trade flows, with no short-term substitutes.

Filling the supply gap is extremely difficult

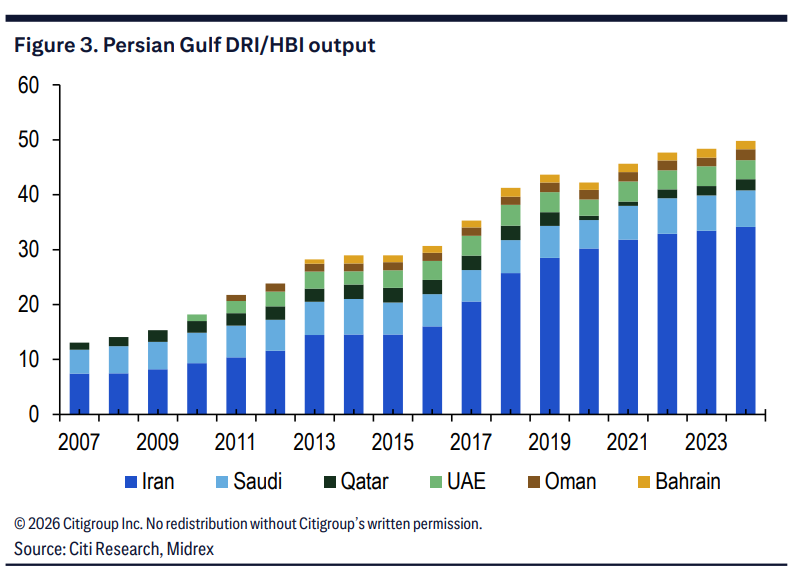

Citi states that Iran’s steel production is highly dependent on gas-based direct reduced iron (DRI) processes, which are entirely different from the global mainstream blast furnace ironmaking pathway, making the difficulty of substitution rise substantially as well.

In 2024, Iran’s DRI output reached 34.2 million tons, up 2% year over year. It is the world’s second-largest DRI producer, accounting for about 69% of total DRI/HBI production in the Persian Gulf region. DRI accounts for only about 7.5% of global crude steel raw materials, yet in Iran, this proportion exceeds 80%—Iran’s steel production relies almost entirely on natural-gas-based reduction of iron ore, not coke smelting.

From a more macro perspective, DRI output in the Persian Gulf region has expanded from 13.1 million tons in 2007 to 49.8 million tons in 2024. Its share of global DRI/HBI total output has surpassed 35% (about 19% in 2007). Iran is the absolute core of this growth.

Once this industrial chain, built on the country’s abundant natural gas reserves, is broken, if other countries want to fill the gap with blast furnace capacity, the raw material structure—from natural gas to coking coal—will undergo a fundamental shift.

Coking coal market: overlooked knock-on effects and a “go long” logic

Citi’s calculations believe that if Iran’s 34 million tons gas-based DRI output is fully replaced by blast furnace capacity in other regions worldwide, it will additionally generate demand of about 20 million tons of coking coal, equivalent to 8% to 10% of the global seaborne coking coal market size.

Even if we only consider replacing the portion corresponding to exports (the coking coal needed for about 9 million to 11 million tons of exported steel products), it would still bring an additional demand of about 6 million to 7 million tons of coking coal.

Of course, Citi research also points to hedging factors: Iran’s domestic steel demand may shrink in the short term under the current situation, so it may not need to replace all DRI capacity in full.

But even if we only calculate the replacement related to exports, the potential incremental coking coal demand of 6 million to 7 million tons is already enough to form a meaningful price-driving force for the relatively limited global seaborne coking coal market.

Focus on three key themes

Citi advises investors to pay attention to three trading storylines: