As the DeFi lending marketplace evolves, the traditional over-collateralized lending model is increasingly revealing its shortcomings in capital efficiency. For institutional borrowers, locking up large amounts of collateral not only raises financing costs but also restricts the flexible use of funds. Consequently, the marketplace is exploring more efficient on-chain credit models that allow institutions to access financing through credit—much like traditional finance—rather than relying solely on high collateral requirements.

Maple Finance stands out as a key innovator in this space. By establishing Institutional Lending Pools, Maple Finance connects liquidity providers’ capital with the financing needs of institutional borrowers, leveraging professional Pool Delegates for credit assessment and risk management.

What Are Maple Finance Institutional Lending Pools?

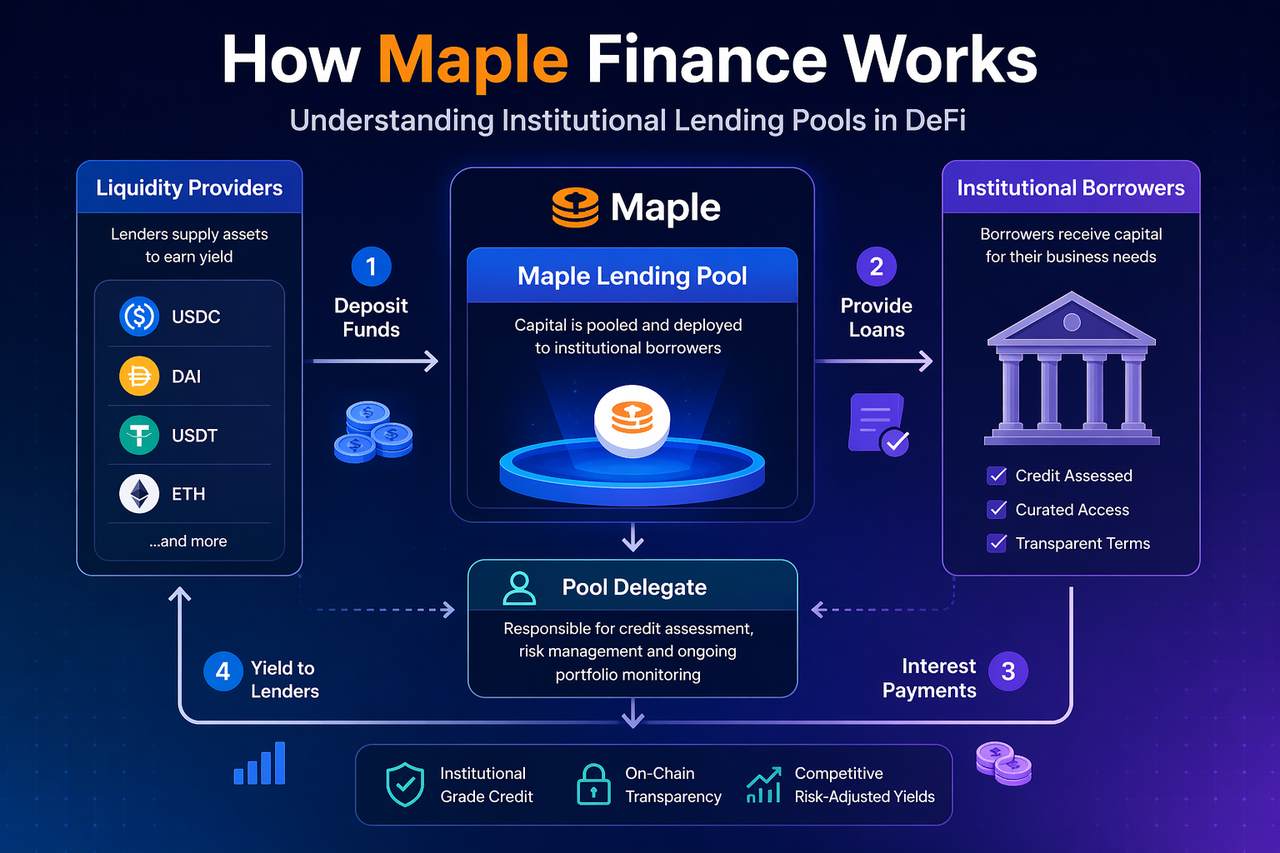

At the heart of Maple Finance lies its institutional lending pool structure—an on-chain fund pool where liquidity providers supply assets and institutional borrowers request loans. Once assets are deposited into the lending pool, they are used to issue loans to vetted institutional borrowers, generating returns for liquidity providers based on the borrowing rate.

Unlike conventional DeFi platforms, Maple’s lending pools are not fully open; instead, they employ professional credit evaluation mechanisms to manage risk. Each lending pool features clear borrowing rules, structured returns, and defined risk parameters, enabling liquidity providers to participate in yield opportunities similar to those found in institutional credit marketplaces. This approach enhances capital allocation efficiency and offers institutions greater flexibility in accessing on-chain financing.

What Role Does the Pool Delegate Play in Maple Finance?

The Pool Delegate is a pivotal figure within Maple Finance’s lending pools, overseeing borrower selection, credit assessment, loan terms, and post-loan risk management. When an institution applies for a loan, it submits financial and credit information to the Pool Delegate, who evaluates its borrowing capacity and default risk, then determines whether to approve the loan.

This mechanism effectively brings the credit intermediary function of traditional finance into the DeFi ecosystem. The Pool Delegate reduces default risk within the lending pool and improves the quality of loan assets. Liquidity providers rely on these professional managers for risk assessment, allowing them to earn on-chain returns with enhanced risk control.

How Does the Maple Finance Lending Process Work?

Maple Finance’s lending process comprises four main steps. First, liquidity providers deposit funds into the lending pool, forming a capital base for lending. Second, institutional borrowers submit loan applications, which are reviewed by the Pool Delegate for eligibility and loan terms—such as interest rate, duration, and amount.

Once approved, the lending pool issues loans to institutional borrowers. Borrowers pay interest during the loan term and repay principal at maturity. The platform distributes interest income to liquidity providers according to preset rules, while the Pool Delegate collects a management fee. The entire process is automated via Smart Contracts, enhancing capital allocation efficiency and ensuring transparent, traceable lending records.

How Does Maple Finance Generate Returns for Liquidity Providers?

Liquidity providers earn returns in Maple Finance by supplying funds to the lending pool. Loan interest paid by institutional borrowers forms the primary source of return, distributed proportionally to liquidity providers. Because borrowers are typically institutions, borrowing rates are generally higher than those for traditional low-risk financial products, offering relatively stable yield opportunities.

Moreover, Maple Finance’s yield model is based on genuine lending demand, not token inflation incentives. This ensures that returns are closely tied to real financial activity, rather than short-term liquidity mining rewards. For on-chain capital seeking stable yields, this approach delivers greater sustainability and appeal.

What Are the Advantages of Maple Finance Lending Pool Mechanisms?

Maple Finance’s lending pool mechanism excels at improving capital efficiency. While traditional DeFi lending relies on over-collateralization, Maple enables institutions to access more flexible financing through credit assessment, allowing borrowers to secure loans at lower capital costs. This model aligns better with institutional fund management needs and brings on-chain lending closer to traditional financial practices.

Additionally, the lending pool structure offers liquidity providers clear sources of return and a robust risk management framework. The Pool Delegate’s professional review process reduces default risk, while on-chain execution ensures transparency and efficiency. By combining expert credit management with DeFi automation, Maple Finance serves as a critical bridge for institutional credit entering on-chain finance.

What Are the Risks of Maple Finance Lending Pool Mechanisms?

Despite the improved capital efficiency, Maple Finance’s lending pool mechanism carries credit default risk. If institutional borrowers fail to repay loans on time, liquidity providers may incur losses. While the Pool Delegate conducts thorough credit assessments, loan defaults cannot be entirely eliminated.

Market liquidity risk and Smart Contract risk are also significant. During periods of high market volatility, exiting liquidity may be restricted, and vulnerabilities in Smart Contracts could jeopardize fund security. Participants seeking yield should carefully evaluate the quality of lending pools, the reputation of Pool Delegates, and the platform’s overall risk control capabilities.

Summary

Maple Finance connects liquidity providers and institutional borrowers through institutional lending pools, leveraging Pool Delegates for credit assessment and risk management to build a more capital-efficient on-chain credit marketplace. Compared to traditional over-collateralized lending, Maple Finance better addresses the financing needs of institutional users and offers more sustainable yield opportunities for capital providers.

As institutional funds continue to flow into the DeFi marketplace, Maple Finance’s lending pool model is poised to become a foundational infrastructure for institutional-grade on-chain lending.

FAQs

What is the responsibility of the Pool Delegate in Maple Finance?

The Pool Delegate is responsible for borrower screening, loan terms, and risk management, acting as the core credit manager within Maple Finance’s lending pools.

Where does Maple Finance’s yield come from?

Yield primarily comes from loan interest paid by institutional borrowers, with liquidity providers earning returns based on their contribution ratio.

How does Maple Finance differ from traditional DeFi lending platforms?

While traditional DeFi lending relies on over-collateralization, Maple Finance utilizes a credit-based lending model, making it more suitable for institutional borrowers and improving capital efficiency.

Are there risks in Maple Finance lending pools?

Yes—risks include loan default, liquidity, and Smart Contract vulnerabilities. However, the Pool Delegate mechanism helps mitigate some of these risks.