The Gate Composite Index (ALL) reflects the overall market performance of USDT-Margined perpetual futures markets, which, to some extent, can serve as a benchmark reference.

Index Components

| Index Name | USDT-Margined ALL Composite Index |

|---|---|

| Contract Symbol | ALLUSDT |

| Index Description | A comprehensive market index of approximately 500 contracts, priced in USDT |

| Initial Index Value | 1 |

Constituent Selection

The Gate Composite Index (ALL) conducts a weekly re-selection of its constituents, dynamically adjusting them according to the latest market conditions to ensure the index accurately reflects current market performance.

Reconstitution Frequency: Once per week

Selection Criteria: Index constituents are selected from all futures markets based on a composite ranking of trading volume, market capitalization, and open interest. 500 futures markets are included in the index.

The Gate ALL index does not include the following futures types:

- Pre-Market perpetual futures

- USDT-Margined delivery futures

- USDT-Margined perpetual futures quoted in USDC or other stablecoins

- Coin-Margined perpetual and delivery futures

- Composite index perpetual futures

- Contracts pending delisting within 48 hours

Index Calculation Details

Rebalancing

Gate Composite Index (ALL) is rebalanced daily at 08:00 (UTC).

During the rebalancing, index constituents are re-selected based on the latest data, and the index price is recalculated. Corresponding parameters, including constituent weights, the divisor, and adjusted price ranges, are updated accordingly. These updated parameters remain effective for real-time index calculation until the next scheduled rebalancing.

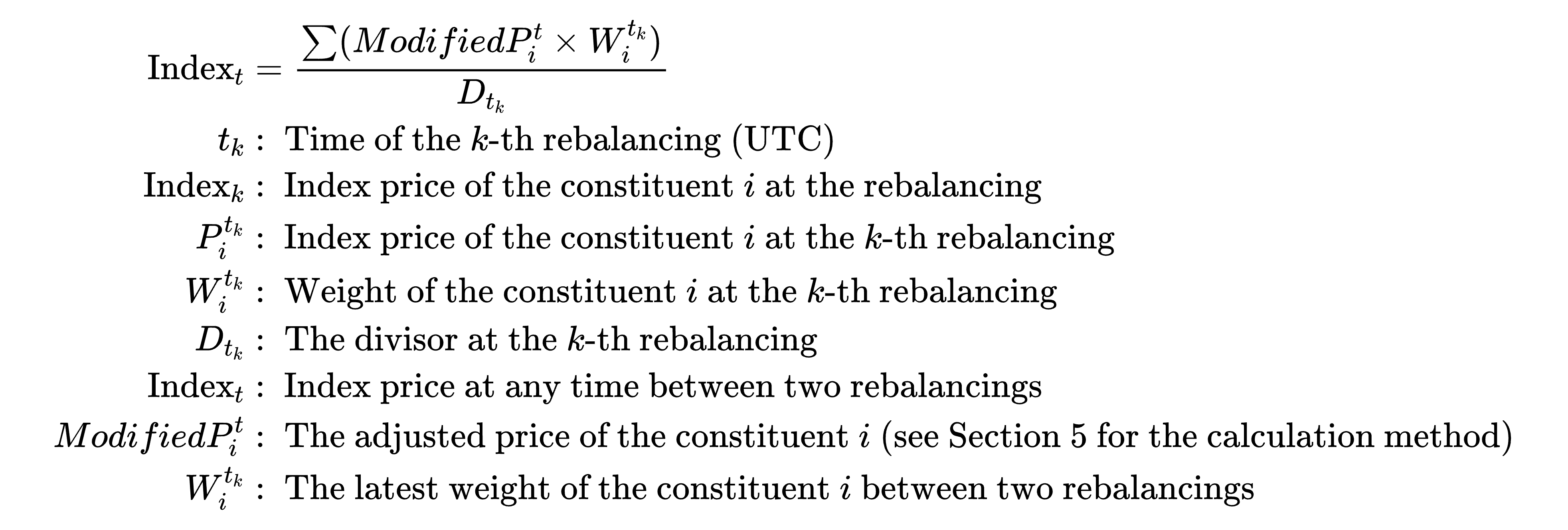

Index Calculation Formula

The index price is calculated under two scenarios:

At Rebalancing:

Example: At the rebalancing at 08:00 (UTC), suppose the index constituents have the following parameters: BTC has a weight of 0.00005 and a price of 10,000 USDT; ETH has a weight of 0.00025 and a price of 2,000 USDT; and the divisor D = 1

The index price is calculated as: (0.00005 × 10000 + 0.00025 × 2000) / 1 = 1

The period between two rebalancing (e.g., from the 𝑘-th rebalancing to the (k+1)th rebalancing):

Example: At the rebalancing at 08:00 (UTC), suppose the index constituents have the following parameters: BTC has a weight of 0.00005 and a price of 10,000 USDT; ETH has a weight of 0.00025 and a price of 2,000 USDT; and the divisor D = 1

The index price is calculated as: (0.00005 × 10000 + 0.00025 × 2000) / 1 = 1

The period between two rebalancing (e.g., from the 𝑘-th rebalancing to the (k+1)th rebalancing):

Example: At 09:00 (UTC), the index constituents are as follows: BTC has a weight of 0.00005 and an adjusted price of 12,000 USDT; ETH has a weight of 0.00025 and an adjusted price of 2,100 USDT, with a divisor D = 1

The index price is calculated as (0.00005 × 12,000 + 0.00025 × 2,100) / 1 = 1.125

Example: At 09:00 (UTC), the index constituents are as follows: BTC has a weight of 0.00005 and an adjusted price of 12,000 USDT; ETH has a weight of 0.00025 and an adjusted price of 2,100 USDT, with a divisor D = 1

The index price is calculated as (0.00005 × 12,000 + 0.00025 × 2,100) / 1 = 1.125

Calculation of Weight Factors and Constituent Weights

The weighting factor of each constituent is

n: The number of constituents included in the Gate Composite Index

Example: if the index has 500 constituents, the weighting factor is

n: The number of constituents included in the Gate Composite Index

Example: if the index has 500 constituents, the weighting factor is

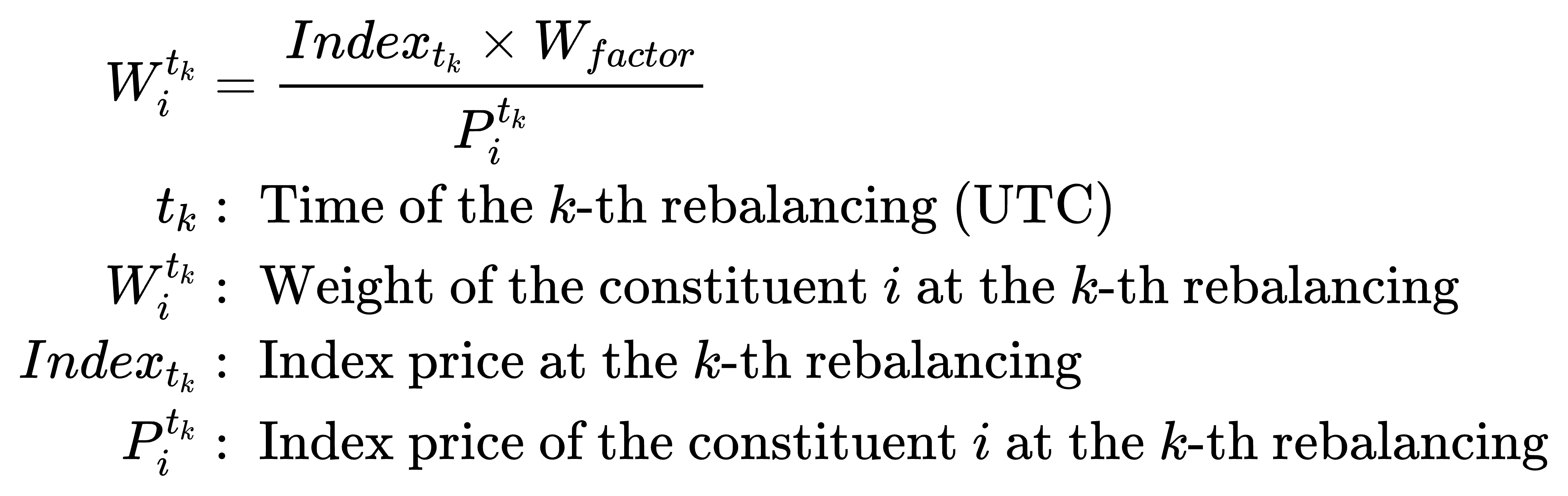

Constituent weight is

Constituent weight is

Example: Suppose the composite index contains 10 constituent tokens, and BTC has a price of $10,000. If the index price at the rebalancing is 1, then the weight of BTC is calculated as:

Example: Suppose the composite index contains 10 constituent tokens, and BTC has a price of $10,000. If the index price at the rebalancing is 1, then the weight of BTC is calculated as:

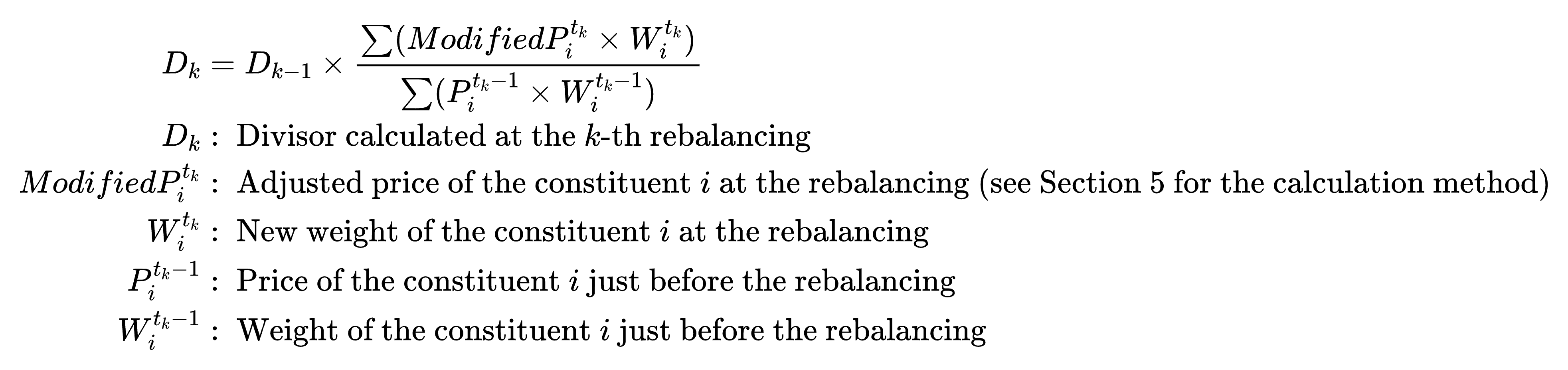

Divisor Calculation

At the initial calculation, the divisor is

At rebalancing, the divisor is

At rebalancing, the divisor is

Example: Suppose the constituent prices and weights before and after rebalancing are as follows:

| BTC Price | BTC Weight | ETH Price | ETH Weight | D | |

|---|---|---|---|---|---|

| 07:59:59 (UTC) (Just Before Rebalancing) | 12000 | 0.00005 | 1800 | 0.00025 | 1 |

| 08:00:00 (UTC) (At the Rebalancing) | 12500 | 0.00004388 | 1820 | 0.000290522 |

The latest divisor: D = 1 × (12050 × 0.00004388 + 1820 × 0.000290522) / (12000 × 0.00005 + 1800 × 0.00025) = 1.007146705

Price Adjustment

To minimize the impact of extreme market conditions on the index, constituent prices will be adjusted.

Adjusted Price is

Example: At a rebalancing time, the price of a constituent is 100. The adjusted price range is [100 × 0.2, 100 × 1.8] = [20, 180]. This means that until the next rebalancing, if the constituent's index price exceeds 180 or falls below 20, it will be capped at 180 or floored at 20 in the index calculation.

Example: At a rebalancing time, the price of a constituent is 100. The adjusted price range is [100 × 0.2, 100 × 1.8] = [20, 180]. This means that until the next rebalancing, if the constituent's index price exceeds 180 or falls below 20, it will be capped at 180 or floored at 20 in the index calculation.

Important Notes

Under normal circumstances, the index is rebalanced daily at 08:00 (UTC), updating constituents, weights, and other parameters to reflect the market changes.

In cases of extreme market events, Gate may conduct interim adjustments.

Extreme market conditions may include, but are not limited to:

- Abnormal price volatility in the constituent, or deviation from similar assets or related markets without a reasonable explanation

- Suspension, delisting, or prolonged trading halt of a constituent on major exchanges

- Erroneous or severely distorted price of a constituent

- Negative news, regulatory risks, or other significant adverse events affecting the constituent

Disclaimer

The content provided herein is for reference and educational purposes only and does not constitute any financial, investment, trading, or legal advice, nor does it constitute an offer or solicitation to buy or sell any digital assets. Gate makes no express or implied representations or warranties regarding the accuracy, completeness, or timeliness of the information contained herein. Product features, interfaces, rules, and fee structures may be updated or adjusted at any time. Please refer to the latest announcements and the actual information displayed on the Gate platform for the most accurate details.

Digital asset investments involve significant risk, and prices may fluctuate substantially. You may lose the entire amount of your investment. Please make decisions cautiously based on your own financial situation and risk tolerance after fully understanding the associated risks. If necessary, you are advised to consult an independent professional financial or legal advisor.

For more information about potential risks, please refer to Gate's Risk Disclosure and User Agreement.